The Sudden Dominance of the Diversity Industrial Complex | RealClearInvestigations

Geneva City Council Agenda Item 4b for February 21, 2023: Consider Draft Resolution Authorizing the Acceptance of a Proposal from Ethos in an Amount Not to Exceed $20,000 for Stakeholder Facilitation to Create a Community Diversity, Equity and Inclusion Plan.

Does every person, family, organization, church, school, small business, and corporation need a DEI plan? Is any federal, state, county, or local government required by law to have such a plan? Does every entity need paid staff to implement/enforce such a plan? Unless all plans are identical, each of us may fall under the guidance of dozens of plans. Was the Geneva DEI expenditure in the budget?

Given that hundreds of thousands of causes are deemed worthy by at least some people, how does an ultralocal political micro-municipality of 20,000 people prioritize its funding? Does the City of Geneva have a policy on this DEI issue and a plan to audit the effectiveness of the tax money spent? Recently funding for the Geneva History Museum was held up by the lack of such a policy. The “feel good” test was decried as insufficient.

Affordability is a necessary, but not sufficient, characteristic of inclusive communities. But without affordability, all ethical questions are moot for those who cannot afford to enter and for those who cannot afford to stay in Geneva. How does this $20,000, plus the future expenditures needed to implement the resulting plan, advance Geneva’s affordability?

The Geneva History Museum Cash Was Under the Shell Marked “Covid” All Along

“The schism created at the Feb. 6 council meeting was not about the respect and appreciation we have for the museum’s work, but the sudden abandonment of good governance principles – witnessed by the attempt to codify funding beyond the current fiscal year for one organization – without a comprehensive discussion on the parameters and protocols of a funding mechanism that addresses potential requests by outside organizations in an equitable fashion,” Burns said.

In February, the Geneva City Council defeated a resolution (the tally was 5 yeas and 5 nays) to fund the Geneva History Museum with $50K of local tax money. Remember, this is the same group that last year gave $75K to a private lobbying outfit in a failed attempt to buy political leverage for their failed Prairie State Energy Campus, a coal-fired earth warmer. But that $75K was based on “good governance principles.”

The Geneva City Council continues down its well-worn path known as the “Geneva Way.” Burns took his ruler and rapped the knuckles of the five aldermen who, in February, wanted to pass a resolution to fund the Geneva History Museum with $50,000 for one year from recurring locally collected tax sources. The resolution would not and could not make the $50K a yearly stipend, as it would have to be budgeted every year. But the resolution made a recurring revenue stream possible. What the resolution would not have done is to require the recipient to kiss the mayor’s ring annually.

The Mayor and his five night-riders, citing “good governance principles,” shut that insurrection down instantly. The Mayor even invoked his only power: voting in the case of Council ties. He brought the hammer down hard on the fingertips of the gang of five mutineers who dared to question his authority. He boldly voted “nay.” Of course, his vote was a free kick at the can. The resolution had already failed since only a majority vote could pass a funding resolution. But while we are on the subject of character, the book of good government principles includes this, “recusal is ethically required when a reasonable person with knowledge of the relevant facts would question his impartiality in the matter.”

The Geneva City Council invokes formal rules such as FOIA, OMA, and even its own ordinances whenever convenient. Of course, the posse comitatus ignores these same rules when necessary to suit their purposes. Then they invoke their first principle of governance: “the ends justify the means.”

Now, in March, the City administration will roll out its favorite tactical manoeuver: the ambuscade. Miraculously, “Covid” (rhymes with covert) non-recurring funds of $51,000 has been found in the back of the small change drawer at City Hall. Federal money is free. The royal ring has been kissed. Crisis averted.

Aldermen Earmark $1.2 Million to Deliver More Coal-Generated Geneva Electricity to an Area Where the Ground Water is Not Potable and Where PM2.5 Will Make the Air Unbreathable

This 720,000 sq/ft warehouse is in the approval process by the Geneva City Council. This building will have 124 truck docks with access from Kirk Road and Fabyan Parkway.

The Venture Park proposal (Venture Park | Geneva, IL – Official Website) is within the area where the groundwater has been contaminated by 1-4 Dioxane. City of Geneva water is now being provided to residents in this area. These residents will now be subjected to another health threat: PM2.5 air pollution from the heavy influx of truck traffic, plus idling diesel engines. The location within the 1-4 Dioxane area could not be worse since the whole area will be downwind, as the wind rose shows prevailing winds blow from the SW. Poor land planning inflicted the well water disaster on these residents – the siting of two landfills. One of these landfills is not engineered and received waste before the segregation of industrial waste from residential. The landfill time bomb continues to tick.

Now, the City of Geneva wants to encourage more development in a brownfield area. The groundwater in the area seeps from west to east. Contaminant plumes move at various speeds. 1-4 Dioxane is one of the racehorses in the stable of cancer-causing landfill toxic plumes. 1-4 Dioxane is considered a “forever” chemical.

The City of Geneva, under the current administration, was duped into signing a disastrous long-term contract with Prairie State Power, a coal-fired generator owned by Peabody Coal (which subsequently declared bankruptcy). Prairie State Energy Campus – Global Energy Monitor (gem.wiki) The $1.2 million Geneva investment in an electric transformer to service growth in a brownfield could help modestly to lower average electric rates in Geneva. At the same time, Geneva awaits the expiration of the long-term Prairie State disaster many years from now. But the transformer is a speculative investment from both a fiscal and environmental perspective. In some ways, the transformer investment doubles down on the Prairie State Power lousy bet.

City of Geneva Capital Spending Budget

As Usual, More Questions than Answers about the Rules of the Shell Game: The Dunkin’ Shuffle and The Emma’s Landing Grift

The City of Geneva’s annual budget document is not an audited financial report. The budget is a planning document. Still, it provides insight into the City’s priorities and planning prowess.[1] The 148-page document contains not a single explanatory footnote, and the puzzling entries and ommissions are plentiful.

FIGURE 1: City of Geneva Budget Summary

A recent Brenda Shory report in the Kane County Chronicle correctly highlights capital spending as a significant component ($14 million) of the FY 2024 total budget, which is 13% higher ($128mil) than FY2023’s $113mil total. And renowned economists debate where inflation comes from? So, an examination of the Capital Projects Funds is in order. “The budget plan proposes more than $14 million in capital projects.” [2]

First, please raise your hand if you understand the ~$75K in the “Foreign Fire Insurance” revenue line. This is a classic Illinois “where’s the peanut” tax. A non-elected “Board” is empowered to expend Foreign Fire Insurance Tax proceeds for the “maintenance, benefit, and use of the Fire Department.” This Board cannot expend tax proceeds for projects not given budget approval by the City Council. The City Council cannot authorize the expenditures of tax proceeds for projects not approved by the Board.

Consequently, the system requires the City Council and the Board to mutually agree on the expenditures. A more transparent line-item title would be “Firemen’s Slush Fund.” Some municipalities have declined to levy this tax because of the “shared” power with a non-elected board. Geneva keeps its snout in the Fire Insurance trough.

As seen in FIGURE 1, Geneva’s Tax Increment Finance districts’ budgets and actual revenues are mystifying. Take TIF #2, for example. The payments for FY years 2021, 2022, and 2023 are $258K, $251K, and $266K [3] are pretty much in line. The 2022 budget called for $992K in TIF2 revenue. The superficial explanation for this is simple if you understand that the East State Street [Capital] Improvement Project has been slated to begin “next year” every year for almost a decade. Of course, the start did not happen again. And about $1.5MIL in Federal CMAQ grant money is sloshing around in the TIF #2 slush bucket. That money appears and disappears like a rabbit in a hat.

Where was the extra $750K that was budgeted stashed? TIF #2 expires this year, yet $852K is budgeted in 2024 and forecasted at $746K in 2025. How does an expired TIF generate $746K? The two TIFs combined had a $2,419,650 revenue “miss” for FY2022. What happened? Where is the footnote that explains this smoke and mirror exercise?

Before leaving page one of the budget, another question is, where is the revenue from SSA #34? This is the Special Service Area for Emma’s Landing. Remember the non-factual “Fact Sheet” the City of Geneva promulgated, which stated that the property tax on Emma’s Landing would be paid:

“Question: Do affordable housing developments pay real estate taxes? If so, are affordable housing developments assessed at the same rate as market-rate developments? Answer: Affordable and market-rate developments are taxed at the same rate as determined by the Geneva Township Assessor.” [4] FACT: LIHTC projects like Emma’s Landing are taxed under an income-based algorithm that results in the actual tax rate of about 1/3rd of the normal” “EAV” assessed valuation algorithm rate. Emma’s Landing passes two-thirds of its EAV along to the rest of the township taxpayers. Of course, zero rates (see Figures 2 and 3) are 100% lower than your property tax rate.

Another example is the Dunkin site at the corner of Crissey and Route 38. The Dunkin owner paid $715,000 for the two PIN number property in 2019. In 2018 the two parcels were assessed at a value of $336049+$103, 411, or $439,460. In 2021 the assessed fair market value was $390,343+97,717, or $488,060, after spending at least $150,000 on remodeling, equipping, repaving, lights, etc. The $850,000 investment was assessed at less than $500,000. The tax bill went from $10,532 to $10,972.60 on the parcel with the building. About 20% of the tax money went into the TIF #3 slush fund bucket. The property was sold for unpaid taxes and then redeemed. This is a mess of Burnsian proportions and will only worsen. Here is a copy of the latest tax bill for one of the Dunkin parcels:

Here is an example downloaded today of a tax file for one of the Emma’s Landing Planned Unit Development affordable townhome parcels:

FIGURE 2: Property Tax Information for Emma’s Landing PUD Lot 3. The dollar amount on Parcel Number 12-08-225-004 is $576,000. But that number was the sale price of the entire parcel, not just PUD LT 3. However, the above file shows the “Property Class” as “8000-Exempt.” The “Tax Status” is listed as “Exempt.” The total tax is given as $0.00.

Below is what pops up when you click on the green box “print tax bill” in the Geneva Township Assessors site for the parcel 12-08-225-004 described above.

Figure 3: The result of clicking on the green “Print Tax Bill” in Figure 2.

Here is a link to the statute that is used to calculate the Illinois Property Tax for Section 42 Low-Income Housing Tax Credit (LIHTC) Projects:

I suspect that none of the ten Geneva City Council Members understood what they were doing when they passed the Ordinance that created Emma’s Landing. At least, I’d like to believe this was the case. The alternative assumption is almost unthinkable. According to records in the public domain cited here, Emma’s Landing did not receive a property tax bill for 2022. The City sold the property in July 2020 for $576,000. The Illinois Housing Development Authority was duped by the City and Burton Foundation into believing the property was donated. (11831 was the IHDA file for Emma’s Landing application – see document below obtained via FOIA from IHDA.) This “donation” ruse raised Emma’s QAP Score in the competition for IHDA grant money. I’d like to believe that the motto “If You Are Not Cheating, You Are Not Trying” is not Geneva’s.

With apologies to the Scottish Bard: “Politicians’ inhumanity to taxpayers makes countless thousands mourn.”

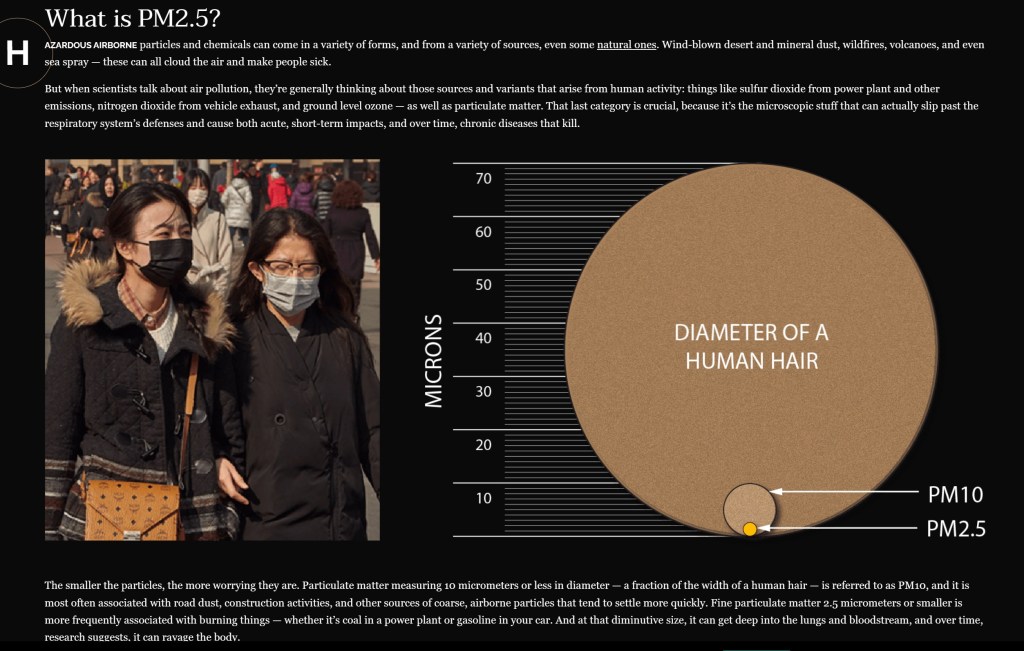

The Short-Term Solution to PM2.5 Particle Pollution is Dilution

The City of Geneva received several years ago a $1+ Million Federal CMAQ Grant to help fund the East State Street rebuild that has been in the planning stage for about two decades. Every year Geneva announces that “next year” is when the project will start. The goal of the grant is to improve diesel fuel efficiency and to dilute diesel emissions as semi-trailer trucks traverse the east side. Route 38 is an Illinois State Designated Class 2 Truck Route. Hundreds of thousands of square feet of warehouses are popping up just to the east. Some of these have been approved by the City of Geneva. Others are in the Geneva system for approval. The PM2.5 pollution problem will increase.

“CMAQ” is an acronym for “Congestion Mitigation Air Quality.” The highest priority is to lower 2.5-micron particles. Please consider going to this website for a few minutes: The Weight of Numbers: Air Pollution and PM2.5 – Undark Magazine Watch the very brief video.

In the 1926 case of Ambler Realty v. Village of Euclid, the U.S. Supreme Court confirmed the legal basis of zoning. The Court recognized that public health protection is the basis of zoning authority, i.e., municipal zoning police power. Am J Prev Med 2005;28(2S2): doi:10.1016/j.amepre.2004.10.028 (activelivingresearch.org)

Geneva’s East State Street Corridor is primarily residential. The parcels that abut the right of way are zoned mostly for mixed uses, but people live in these one-lot deep ribbon zones, such as B3E. Residential zoning is directly adjacent.

What has the City of Geneva done to protect East Side corridor residents? The answer is that the City has repeatedly and consistently made the wrong decisions. The Burns Dunkin at the top of the east side hill is Exhibit A.

No place exists within the City of Geneva that is more ill-suited for high intensity use during peak traffic hours than the corner of Crissey and East State. The mayor snatched defeat from the jaws of victory when he broke the 5-5 tie that would have doomed the project. Fortunately, the ineptness of the applicant and the mayor’s handpicked staff has now delayed the opening for about five years. No one thought to get an IDOT permit that was required before the construction could legally begin. Or did both parties simply hope that would get away with the “mistake”? Mayoral addiction to TIF spending was the root of the problem.

Harry Chapin’s proverbial “thirty thousand pounds of bananas” were terrifying going down the hill into Scranton, PA, in 1974. Stopping the bananas halfway up the east side hill in 2023 and then having to begin the climb anew in first gear is even more terrifying.

Then another high-intensity use (written into the zoning ordinance for the benefit of one applicant) that generates congestion and PM2.5 pollution was spot-zoned for the Geneva Pharmacy so that TIF money could be again squandered. That business folded in less than a year.

When the first principle (dilution) of short-term mitigation of PM2.5 exposure demands more setback from the source, not less, the City granted a variance for Malone funeral home’s new parking lot that reduced the required ROW setback from thirty feet to eight feet. Then the Special Use Ordinance 2021-13 required mandate for asphalt was switched to concrete without the Municipal Code required City Council approval. Due to the localized thermal inversion created by the high albedo (colder/heat reflecting) cement, the PM2.5 particles will be trapped and transmitted to nearby homes and yards. The low albedo (warmer/heat absorbing) black asphalt would have had the opposite effect of diluting and dispersing the PM2.5 particles away from the ground.

Recently the Geneva City Council approved a plan to gift $1.5 million in TIF funds to the Mayor of Naperville to build a retail outlet/high-density multistory affordable residential building with the only access/egress being Crissey directly across a substandard width street from the Dunkin exit. This, too, will require spot zoning and setback variances to move the future residents even closer to the PM2.5 source just outside their open windows. And it will add even more congestion at Crissey and E. State. Absurdly, the City will give away more money to exacerbate air pollution exposure than it received from the Feds to mitigate that same air pollution.

Other examples of bonehead aldermanic and mayoral decisions largely driven by Tax Increment Financing Addiction Syndrome (TIFAS) could be raised.

Longer term, the promise of electric vehicles could reduce PM2.5 particle pollution. But young children are particularly vulnerable, as are older people and those with chronic illnesses. For now, the City of Geneva needs to stop trying to injure those whose health and welfare it has sworn to protect through its zoning police power.

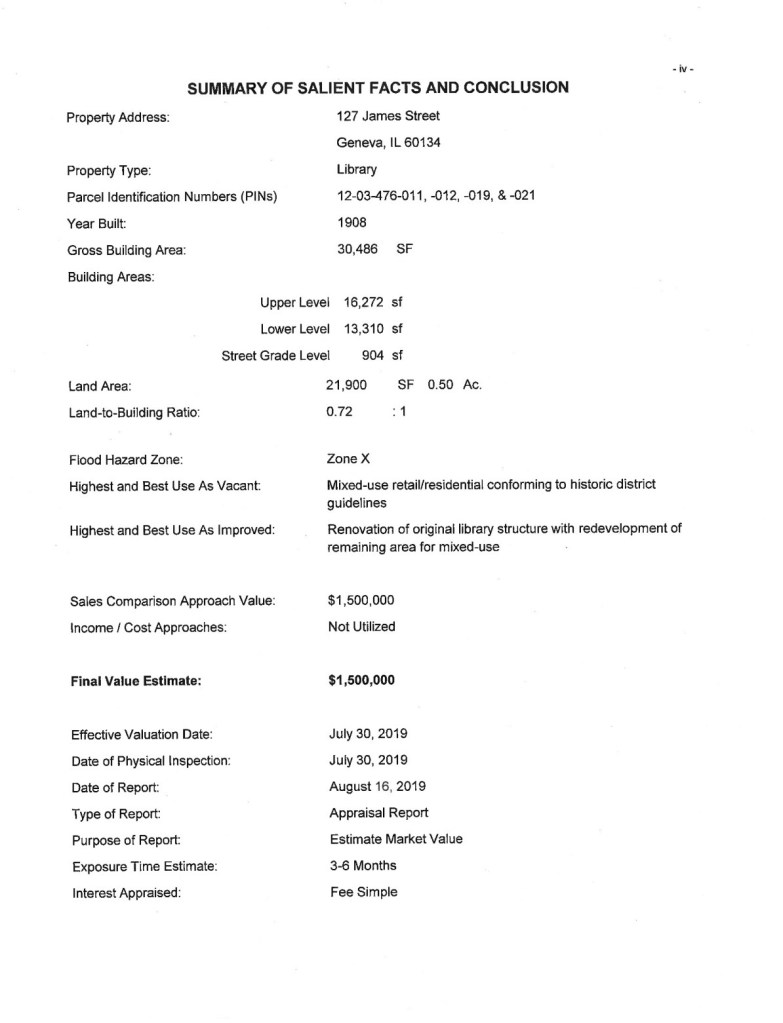

The Geneva Public Library District (GLPD) placed a referendum on the ballot in April of 2017 asking voters to approve a new $21.8 million bond issue to build a new library on the site of the old Sixth Street School. The referendum passed by 96 votes with a 32.5% voter turnout of 7705. No one asked for a recount.

Results of the April 2017 Geneva Public Library District Referendum

The purchase of the Sixth Street School had its share of drama. The Library Board initially said it would hold a referendum on the purchase. Then the board had enough spare change lying around to offer the County $1.5 million plus $300,000 for demolition. The price “drifted” up to $1.8million and the demolition cost to $450,000 because of asbestos and an underground storage tank (both problems were known to be present for at least a decade). https://www.dailyherald.com/article/20150327/news/150329040/

The cost of the new 57,000-square-foot library was substantially north of the $21.8 million in bond receipts (not to mention the interest on the bonds). The GPLD wants to “transfer” the old library at 127 James Street to the City of Geneva for $450,000. The City of Geneva has not proffered a budget for remodeling and maintaining the new 30,000-square-foot space. Apparently, the $450K will come from spare change the City has found lying around.

But is the transfer ethical or even legal? Three Illinois statutes seem important: one authorizes transfers between municipalities but does not mention payments, another Act creates the statutory basis for the existence of Library Districts such as the Geneva Public Library District, and a third act sets out the general rules for the sale of publicly owned real estate.

The Act that authorizes Public Library Districts in Illinois ((75 ILCS 16/) Public Library District Act of 1991) contains these definitions for the purposes of the Act:

“District” means a public library district established under this Act and includes a proposed public library district.

“Library” means a public library, including one privately endowed or tax-supported or one established under this Act. “Municipality” means a city, village, or incorporated town.

The Act that authorizes local government property transfers (50 ILCS 605/) Local Government Property Transfer Act contains this definition:

The term “municipality” whether used by itself or in conjunction with other words, as in (a) or (b) above, shall mean and include any municipal corporation or political subdivision organized and existing under the laws of the State of Illinois and including, but without limitation, any city, village, or incorporated town, whether organized under a special charter or under the General Act, or whether operating under the commission or managerial form of government, county, school districts, trustees of schools, boards of education, 2 or more school districts operating a cooperative or joint educational program pursuant to Section 10-22.31 of the School Code, sanitary district or sanitary district trustees, forest preserve district or forest preserve district commissioner, park district or park commissioners, airport authority and township.

Notice that the Library statute does not define a Library District as a “municipality” and for “purposes of the act” the act narrowly defines “municipality.” By its plain language, the Library Act does not give Library Districts municipality standing to participate in transactions permitted by the Government Property Transfer Act. The Transfer Act contains a very lengthy list of eligible “municipalities,” including Park Districts. But the list does not contain “Library Districts.” The Loophole-Louey at City Hall employed by Mayor Burns will point to the phrase “but without limitation” as their loophole. But the City Code requires that when two provisions apply to a given matter, the more restrictive provision “shall [defined in the code as “must”] govern.”

A couple of other library districts in Illinois have taken a bite out of the property transfer apple. Has anyone challenged their action? Does the applicable city code in those cases contain the “most restrictive shall govern” clause?

A two-party political system is ugly and difficult to watch, very much like professional wrestling. Geneva’s Burns’ single-party system is even less attractive and much more expensive to watch than the WWE. And, just like the WWE, the fix is in. What about a referendum? Or, at the very least, a public auction of the old library and let Mr. Fritz send the new owner a property tax bill?

Rules for a Public Auction of the 127 James Street Old Library

The Transfer Act is silent on the price of the parcel being transferred, so it will be asserted, perhaps correctly, that the City is not required to pay anything. If so, how did the $450K come into play? I do not recall the GPLD divulging during the referendum campaign that the gifting (or selling for a nominal sum) the old library was part of the plan. Who negotiated the $450K, and on what authority? By voting for the library referendum, Geneva taxpayers may have forfeited the property tax income from the old library. And the “yes” voters may have unknowingly granted the City a blank annual check to remodel and carry the expenses of a “new” City Hall that is three times bigger than the current City Hall. The Library Board (unwittingly) snuck in a perpetual tax liability as a reward for (narrowly) passing its $21.8 million request.

(65 ILCS 5/11-76-4.1)(from Ch. 24, par. 11-76-4.1) Sec. 11-76-4.1. Sale of surplus real estate. The corporate authorities of a municipality by resolution may authorize the sale or public auction of surplus public real estate. The value of the real estate shall be determined by a written MAI certified appraisal or by a written certified appraisal of a State certified or licensed real estate appraiser. The appraisal shall be available for public inspection. The resolution may direct the sale to be conducted by the staff of the municipality; by listing with local licensed real estate agencies, in which case the terms of the agent's compensation shall be included in the resolution; or by public auction. The resolution shall be published at the first opportunity following its passage in a newspaper published in the municipality or, if none, then in a newspaper published in the county where the municipality is located. The resolution shall also contain pertinent information concerning the size, use, and zoning of the real estate and the terms of sale. The corporate authorities may accept any contract proposal determined by them to be in the best interest of the municipality by a vote of two-thirds of the corporate authorities then holding office, but in no event at a price less than 80% of the appraised value. (Source: P.A. 88-355; 89-78, eff. 6-30-95.)

Does the GPLD have a valid appraisal of $562,000 for the 127 James Street property? This is the lowest appraisal that would make a sale of price $450,000 comport with the above statute. Proper notice is mandatory, and a 2/3’s yes vote of the Library Board is required (5 yes votes). Has an appraisal been done? Where is the required resolution? How would a “yes” vote be fair and ethical to those library district taxpayers who do not live in the City of Geneva?

The Last (August 2019) Certified MAI Appraisal of the 127 James Street Old Library Property was $1,500,000

In 2018, The City of Geneva had No Interest in the Old Library

Slow down! Thursday night, the Library Board is to vote to “sell” the old library to the City of Geneva for $450K. This will put the City of Geneva taxpayers on the hook for renovations and expenses and potentially take $1.5 million off the tax rolls. The 2018 Burns letter claims “no further interest” in the building, but a secret last-minute deal is about to be cut. Why is the Library Board donating $1 mil to Geneva City Council? This is madness that begs for a more complete and transparent public vetting. A public auction of the property or a referendum are both paths to open, honest government. The current path is the Geneva Way – ambush the taxpayers.

The City of Geneva will buy the old Library for half its advertised value, but don’t get excited. The Geneva Public Library (GPLD) taxpayers are the sellers.

Ambuscade: a high-sounding political tactic that is employed by elected bushwhackers. Example: “The Geneva City Council will stage an ambuscade on Monday evening.” See also: Charette.

Proposed prototype for new Geneva City Hall to be constructed at 4 E. State Street. Note the remnants of the Alexander-Rystrom Blacksmith Shop repurposed as a fence. Landscaping is minimal maintenance. Why did not the $300,000 Charette come up with this obvious solution? A Verizon Cell Tower Tree can be seen on the horizon on the site of the old City Hall..

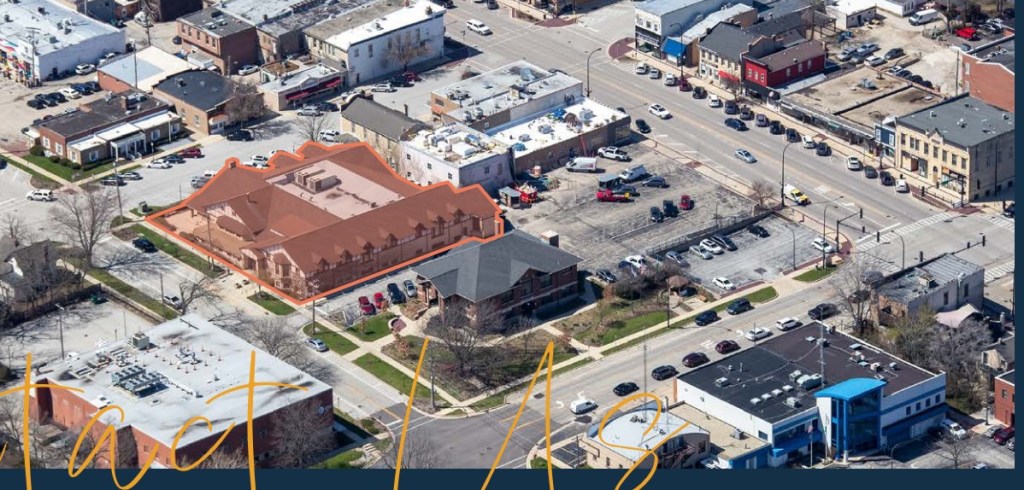

Geneva’s population in 2020 (21,393) was slightly down from 2010 (21,495) per the U.S. census. The Geneva City Council is poised to add half an acre of land and over 30,000 square feet of building for city government tax-exempt use. https://www.geneva.il.us/AgendaCenter/ViewFile/Agenda/_01232023-2079 This will come in the form of a purchase of the Geneva Library District’s abandoned property at 127 James Street.

The price is set at $450,000, going from the City of Geneva’s taxpayers’ pockets into the Geneva Library District’s taxpayers’ pockets. The asking “retail” price for the old Library is $925,000. https://www.cbre.com/resources/fileassets/US-SMPL-78947/ba029964/80f7262f-9cea-4c2e-812d-6465b62e2a4a.pdf As always, winners and losers will be created when politicians act. Library District taxpayers who do not live in the City of Geneva will be modest winners because the money that goes into their pocket does not come out of their other pocket. For City of Geneva taxpayers, there will be off-setting effects since they also live in the Library District.

But what if the property is actually worth ~$900,000? Answer: everyone loses.

The City Hall campus will consist of the architecturally grotesque building with the blue-roofed towering vestibule in the lower right that once was police and fire and now police only except for the western part, the historic City Hall, and the highlighted historic stone library. This photo gives a sense of the massive expansion of municipal government space represented by the ~30,000-square-foot, two-story library.

Over a decade ago, the City agreed with the Library that it could purchase the 127 James Street building after the Library moved to the Cetron Building. Icons for Sale: https://patch.com/illinois/geneva/icons-for-sale-future-of-city-hall-is-anyones-guess The Cetron deal never happened. But at that time, the City estimated that its requirements could be met with 20,000 square feet. The current City Hall was said then (2011) to be 10,000 square feet. It has not changed. (The City’s Finance Department is domiciled with the Police Department across the street from City Hall at 15 S. First Street.)

The new GPLD library is 57,000 square feet, about twice the size of the James Street building. One cannot help but notice a complete set of the Encyclopedia Brittanica (32 volumes in the last print version of 2013) is 4.75 gigabytes. Two hundred complete sets will easily fit on a 1TB thumb drive ($30.00 on Amazon now). The moral of this might be that if you need to know how extensive a library you need, don’t ask a librarian.

If the City of Geneva purchases the 127 James Street Library, the City will have 40,000 square feet. With the same population over a decade ago, the City estimated its need at 20,000 square feet. Geneva had ten alderpersons then and ten alderpersons now. In 2021 the City of Geneva had 121 employees. Eight years ago, the City had 128 employees. City of Geneva Salaries – Illinois – 2021 (govsalaries.com)

Why does the City of Geneva need 40,000 square feet of buildings? Why should 30,000 square feet in the heart of downtown with a $925,000 asking price be taken off the tax rolls? Why does the proposed transaction show up on Friday, January 20, 2023, with the vote to come in a Special (unscheduled) session on Monday, January 23, 2023?

Why doesn’t the $450,000 go towards cleaning up the old MRI site at 4E State?

PS: As part of its series on “concepts in government,” the next GPLD board meeting will start with a brief presentation on “Fiduciary Responsibility.”

The Mill Race Inn site is a brownfield, but no one wants to talk about it. Jabberwocky rules Geneva by stuff and nonsense.

Dear Neighbors:

Attendees of the City of Geneva Historic Preservation Commission meeting on Wednesday evening, January 18, 2023, were enlightened about a limited set of the controversies surrounding the ca1846 old rubblestone core of the Mill Race Inn, also known as the Alexander-Rystrom Blacksmith Shop.

The meeting started at 7 pm playing to a full house. The agenda had four items, with the public hearing over the Mill Race stone ruins at the top. Chairman Zellner, a dedicated volunteer to the cause of preservation, dutifully, if not eloquently, read the proforma ground rules. This recital took thirty minutes off the clock. Then we were told the hearing would end at 8:30. The “ground rule” that caused me to sigh (inaudibly, I hope) was Code, Section 10-6-10.A9: “the merit of any proposed replacement construction or improvement shall not be a standard of review for a demolition request.” The assembly gathered to weigh the destruction of a formally landmarked historical structure against an unknown. This felt akin to having the sheriff show up at my door to inform me that I had to decide whether to move out of my house by Tuesday next. However, any thought of where I would end up if I chose to leave is strictly prohibited and must not enter my mind.

Then, the congregation was informed that the HPC had already determined the question of landmarking based on historical significance affirmatively. So, tonight was not the night to drag history into the discussion. Here, verbatim, is the agenda item as it appears on the City’s website: “Demolition of a Historic Landmark and De- De-designation of the Property.” My first reaction when I read this was, “huh?” Was this a move to re-designate the entire site as a landmark (which should happen, IMHO)? Or was this a Freudian typo? First, demolish and then de-designate? Then I remembered my Alice:

‘No, no!’ said the Queen. ‘Sentence first—verdict afterwards.’

‘Stuff and nonsense!’ said Alice loudly. ‘The idea of having the sentence first!’

‘Hold your tongue!’ said the Queen, turning purple.

‘I won’t!’ said Alice.

Off with her head!’ the Queen shouted at the top of her voice. Nobody moved.

‘Who cares for you?’ said Alice, (she had grown to her full size by this time.) ‘You’re nothing but a pack of cards!’

Mr. Patzelt, the Shodeen representative, spent most of the remaining allotted time shredding the Geneva professional staff’s work into confetti. (OK, I admit it, this brought a smile, if not a grin, to my face.) In summary, the meeting was somewhere between a hog-calling contest and a Masonic ritual.

Based on the complete lack of information about the development plan, I had planned to speak in favor of preserving the ruins. After all, the Sandborn Map of 1891 “designated” the structure with only the word “ruins.” Yet the “ruins” became Geneva’s most identifying structure for most of the following century. Anyone who ever dined in the Stone Room knows of what I speak. January 2011 was our last meal there. The Grecian chicken was superb (matched in Geneva only by Munchie P’s.) The first time I ate in the Stone Room was in 1953.

Plus, one of the contexts that determine historical significance is what happened at the site. In this case, the ruins mark the spot where a small gap between Big Woods and Little Woods coincides with an island refuge in the river and a natural limestone ford at the head of the island. Our national mammal, the American Bison, discovered that ford as early as 400,000 years ago, give or take. 15 Facts About Our National Mammal: The American Bison | U.S. Department of the Interior (doi.gov) The ford was the river crossing of an interstate highway, a buffalo trace, that took the buffalo “over the river and through the woods” on their way from the tall grass prairies of Illinois to the salt licks of Kentucky and back. As the American Bison went, so did America’s indigenous peoples.

Daniel Shaw Haight knew the Geneva site in Sandusky Precinct was valuable for precisely the same reasons that the Alexander brothers did. Haight sold out to Herrington because he found nearby an even more promising river and ford with hydropower. He founded Rockford. He and his legendary oxen built the first structures both here and there.

The MRI saga will air another episode on about the Ides of March. Stay tuned; maybe the band from Berwyn will play then.

Reports on social media that the CVS pharmacy at State Street and Bricher Road (1500 Lincoln Hwy. Saint Charles) is closing on February 1, 2023, have not yet been confirmed by a press release. CVS announced in 2021 a plan to close about 10% of its stores over the following three years, so the reports are ominous. CVS Closing Hundreds Of Stores: Will IL Locations Survive? | Chicago, IL Patch

For background on the Geneva pharmacy situation, please see:

“Geneva Pharmacy” at 501 E. State St. in Geneva failed in less than a year despite a $100K gift of Geneva taxpayer TIF money, plus the usual “Geneva Way” rewards of spot zoning, etc. The cash was not subject to a claw-back provision. Stand-alone pharmacies do not generate much local sales tax revenue, as prescription medicines are not subject to local sales tax. Companies like CVS derive most of their revenue and about two-thirds of their profits from prescription medicines. CVS has partnered with Target to house its prescription services. St. Charles, for example, is listed as having two CVS stores and Batavia and Geneva one each. Soon, if the reports are true about the west side CVS closure, only Geneva will have a non-Target housed CVS.

This may be a classic example of the adage “It’s better to be lucky than smart” when it comes to the Geneva City Council’s decision to provide taxpayer-funded subsidized competition for its CVS. Geneva’s east side CVS may capture some store traffic because of the closure of the west side store.

Contention on the waterfront is nothing new in Geneva, but we are moving backward without governmental cooperation or leadership.

Geneva in 1872 superimposed on today’s Geneva. Note how the RR Bridge of 1854 was half dam and half-bridge, cutting the tail off Herrington’s Island and leaving the east side with the stench. The original U.S. Survey in 1841 (begun in 1839) showed the east side channel was the same width as the west side. Please see: Back to When the River Made Pearls, not Stenches – Rod’s Ramblings and Ruminations (genevanotes.com)

The old stone structure at the eastern foot of the State Street bridge that was the core of the Mill Race Inn restaurant had many uses going back to the 1840s.

The present-day rubble stone ruins of the Mill Race Inn have a legacy that includes carriage painting on its roof, which has left lead pollution of unknown quantity and persistence. The site is a brownfield: a former industrial or commercial site where future use is affected by real or perceived environmental contamination. Merriam-Webster.com Dictionary, Merriam-Webster, https://www.merriam-webster.com/dictionary/brownfield. Accessed 9 Jan. 2023.”

Unfortunately, “micro-brownfields” exist scattered throughout most municipalities. For example, small rubbish “pits” were prevalent in Geneva. Industrial areas often disposed of coal bottom ash and cinders on-site and used it for fill.

Geneva Republican June 21, 1929, p.1.

The MRI ruins have some historical significance, but the surrounding context now is far different than 180 years ago. Last spring, the City Council severed the ruins from the rest of the historic site once known as Thompson’s Woods, a place immortalized in the poem of that name by Forrest Crissey. This was a lethal wound. Without context, the structure’s future value became permanently impaired. The first blow to the ruin’s historical context was struck in 1854!

The 1854-1883-1920-1961-2022 Geneva railroad “bridge” was (and is), in reality, half-bridge and half-dam. Bridgehunter.com | UP – Fox River Bridge (Geneva) (1920) The eastern Fox River channel was dammed in 1854 by the east bank bridge buttress, which cut off the lower third of the original Herrington’s Island. The eastern channel of the river below the RR bridge to the south was thus turned into a backwater slough, which was landfilled for about 100 years as a dump (mostly with mercury-rich coal bottom ash and cinders). Well into the 1950s, the municipal waste stream was binary: rubbish and garbage, the former being dry waste not readily decomposable. Garbage dumping was not permitted in the City of Geneva dump-in-the-slough. Geneva was heated and lit with coal, making coal bottom ash and cinders a large percentage of its “rubbish.” Later the slough was used as a shooting range, adding lead to the mercury contamination. The eastern channel was diverted back into the Fox River above the east bank buttress, but it has silted in, which changed the course of the river by erosion of the west bank.

Rubbish was cheap fill, hence the above in the Geneva Republican Dec 13, 1904, p4.

An attempt in the early 1960s was made to “re-balance” the two channels around the remaining portion of Herrington’s Island by re-opening the old mill race (which had been filled mostly with coal bottom ash and cinders) using a large pipe and a ditch that ran from above the Geneva dam to just below the State Street Bridge and into the east channel. This worked to keep the east channel from becoming a stagnant water source of foul odor. But the State of Illinois ordered the ditch closed in 1964, and the odors returned – the river is much cleaner now than it was in the last century. Geneva Attorney (and folk hero to many) Roy Lasswell, (1924-1987), retained by the east side homeowners disgusted by the stench, blocked the bulldozer with his Volvo station wagon in 1964 to prevent the destruction of the balancing bypass of the dam. He was arrested.* See the Geneva Republican February 27, 1964, p1. https://box2.nmtvault.com/Geneva/jsp/RcWebImageViewer.jsp?doc_id=9351816b-0b6a-40e9-9d50-bf1f22f4eedf/gn000000/20221210/00000217

Often, coal ash wound up in the street. Geneva Republican November 3, 1893, p3.

Earlier and gradually, the width of State Street was increased, and the grade was altered by cutting into the east side hill and raising the grade leading up to the bridge. As a result, the rubblestone ruins site lost much visibility and historical context. Its vernacular industrial architecture was often altered since its original construction. And the building was often vacant for extended periods. Structural integrity was cut to shreds by added fenestrations. The 1872 Kane County Atlas map of Geneva depicts that modern Crissey Avenue was then named Batavia St., and Bennett Street/Route 25 did not exist. The ruins were on the northwest edge of Thompson’s Woods, with George Thompson’s apiary the most well-known enterprise, and his honey much sought after.

Geneva has become obsessed with preserving the ruins, while the 1.8-acre riverfront site itself is the prize that should be coveted. Geneva is ignoring the brownfield status of the entire site. What is urgently needed is an environmental survey like that done at Shodeen’s proposed 1 Washington Place in Batavia. (After five years of planning and two failed TIF Districts, Shodeen pulled out of that project precipitously a year ago.) The City of Batavia owned the property and spent more than $500K on environmental remediation, including lead and mercury.

The uses on or near the MRI brownfield site were, just like in Batavia, sources of both mercury and lead plus petrochemicals and asbestos. One must not forget that the massive Bennett Mill mysteriously burned to the ground in 1971 (3129) GHM Minute: Bennett Mill: Geneva, IL – YouTube. The structure was brick, but lead paint was used widely on the interior and exterior. A “lead ash halo” was created, and the post-fire ash and rubble were simply plowed into the foundation, and never excavated. Arson is a dark recurring thread in Geneva’s historical fabric. The Howell Foundry on the west bank moved to St. Charles after a fire believed to have been set by an arsonist. A former Geneva village president’s barn suffered the same fate.

Other brownfield uses included lead paint spraying, a cinderblock factory (cinders=coal bottom ash rich = mercury), an automotive dealership with a garage (asbestos and lead), an auto radiator repair shop (lead), two gasoline stations (lead and petrochemicals), and, of course, fill was used that was often coal fly ash (mercury). The Bennett Mill ran on coal/steam much longer than on hydropower.

Fly ash (airborne) and bottom ash (falls to the bottom of the boiler) are considered environmental hazards worldwide since they generally contain organic pollutants, and probable toxic metals like Se, As, B, V, Al, Pb, Hg, Cr, and radionuclides Uranium, Thorium.

Unfortunately, many of these uses were “grandfathered” out of modern environmental requirements such as Leaking Underground Storage Tank regulations (pre-1974 uses are exempt). Environmental lead has a dissipation half-life of about 600 years. Under Illinois’s TACO, leaking storage tank rules, problem sites are often “papered over” and not remediated. Both East and West State Street are riddled with old gas stations that have not been mitigated. No one knows how many underground tanks remain. Don’s Gas-For-Less at State and East Side Drive Aldi is an exception that cost the city several 100K$ in TIF funds. Airborne lead now is the major route for childhood ingestion in the U.S.

Ironically, Geneva went from coal (mercury) to leaded gas (lead) to diesel (sub-2.5-micron particles) along Route 38 (State). Route 38 is a State designated truck route! Geneva put a Dunkin’ at the top of the hill on a LUST (leaking tanks)/TACO (Tiered Approach to Corrective Objectives) site where residential uses are prohibited by IEPA, as recorded on the deed! But minimum wage kids can work 12-hour shifts on the site. Geneva’s aldermen approved a drive-thru at the top of the hill (the vote was 5-5, with Mayor Burns breaking the tie with his yes vote creating the “Burns Dunkin'”) that will stop the diesel trucks coming up the hill. A stopped 40,000-pound load needs a lot of diesel fuel to get back up to 30 mph, especially up a hill. This is after Geneva received $1 mil in Federal CMAQ (congestion mitigation/air quality) grants to improve diesel efficiency and air quality along East State Street!

Another consideration, albeit a bit tangential, is that the Geneva dam will likely be removed in the not-far-distant future. Please see Back to When the River Made Pearls, not Stenches – Rod’s Ramblings and Ruminations (genevanotes.com). The advantages and disadvantages of dam removal are discussed by the “Friends of the Fox” here: Frequently Asked Dam Questions | Friends of the Fox River. Removing the dams will make the Fox River friendlier to canoeists, kayakers, and fishermen. “Clamming” (and pearls) might even come back. The City of Geneva and the Geneva Park District should seriously consider how the increasing demand for access to the river will be met. If the river becomes a rafting, canoeing, kayaking “highway,” an enter/exit/rest-stop in the heart of downtown Geneva could also be an economic/tourist booster.

I do not oppose the redevelopment of the old MRI site. However, I am for doing it right. Lead, mercury, asbestos, petrochemicals, etc., pose a potential risk to current and future residents. Disturbing the site, a brownfield based on its prior uses could put contaminated dust in the air for current Geneva children to inhale. This is not covered by the current permitting process, which does not mandate heavy metal testing, For example. examine how Batavia handled a nearly identical scenario on its old industrial site on the east bank of the Fox. As the property owner, the City did a thorough independent environmental assessment beyond what was “covered” by the permitting process. Batavia found contaminants (including lead and mercury) and mitigated the site with IEPA guidance.

Notice that even though the developer (Shodeen) walked away at the very last moment, the Batavia site is now green and neat and kept that way. Unfortunately, Batavia lost a historic church but did not leave the foundation as a gaping, water-filled hole. Geneva’s similar site is a disgrace and an embarrassment to its citizens. See, for example, Kane County Chronicle, 2019/02/25: “Batavia aldermen ok lead cleanup plan: While aldermen have been sharply divided on the redevelopment project itself, they closed ranks to approve the cleanup plan, saying they essentially had no choice.”

The Geneva aldermen refuse to remove their blinders lest they catch a glimpse of the potentially serious problems they have repeatedly and irresponsibly chosen to ignore.

The Mill Race Inn River Room just prior to the start of the Great Recession in 2007. New owners took over the MRI in 2004. They never recovered from the flood of 2007, when they lost $35,000 worth of food and liquor. Their former restaurant, Horwath’s on Harlem Ave., also had some misfortunes, such as when a bomb went off inside on May 4, 1982, with only the owner inside. Photo gallery: A history of Elmwood Park — Chicago TribuneThe old Geneva dam in 1939 versus the 1961 dam as it appeared in 2014. The problems in the early 60’s with stench were caused by the loss of the mill race.

* Attorney Roy Selleck Lasswell, an east sider, lived at 860 N Bennett Street near Division in Geneva just south of the St. Charles line. He was a graduate of the Northwestern School of Law and served in the U.S. Navy as an LTJG in WW II. I had the privilege of knowing his wife, Carol, a court reporter. Roy’s father, Tull C. Lasswell, was also an attorney. In 1962-3 Mr. Lasswell was the Geneva City Attorney. He expressed pride in the Geneva Plan Commission. In the mid-70’s the Lasswell’s moved to Batavia.

Roy Lasswell’s home is near the east bank of the Fox River next to Riverside Park on the Fox River Trail.

{kind=link}