Please read Mike Lambert’s (a City of Geneva superstar and architect) 2021 description of the building’s storied and controversial history and its life-threatening flaws.

The new jack-of-all-trades Geneva Fire Department Ford F150 Lightning pickup truck may be the command vehicle, but it commands no respect. As per the usual “Geneva Way,” the process was hidden from public view using a barrage of agendas and the usual ambush scheduling.

The Crissey/State Dunkin Special Use Permit (Ordinance 2018-36) has an approximate cash value of $250,000. Not a bad return on a speculative grift. But the City of Geneva has been an easy mark for scammers for two decades. The Prairie State Energy Campus is the granddaddy.

The Leaking Underground Storage Tank Property at 206 E State is uninhabitable for residential use. If the reader goes to the Kane County Recorder’s site and enters document 2017K018663, the reader will find an IEPA “No Further Remediation Letter” that contains this restriction on the use of the land: “limitation: The land use shall be industrial/commercial. The groundwater under the site shall not be used as a potable water supply.”

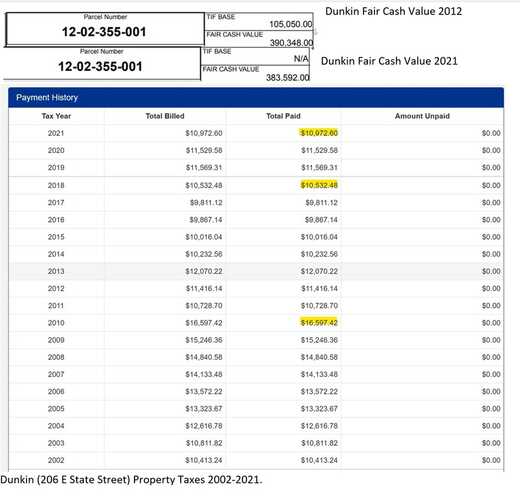

Below is the fair market value of the Dunkin site in 2012 and 2022 and the actual taxes paid from 2002 to 2021. The Hari Group actually skipped paying property tax for a while but bought the property back after it was sold at a sheriff’s sale. Here is the timeline:

2017: Property first becomes saleable for commercial industrial use after TACO review and NFR;

2018: On Nov. 18 City grants a Special Use Permit to the Hari Group, Inc., for a drive-through. This Special Use Ordinance is unlawful under the Geneva Municipal Code, which states, “C. Initiation: The owner of the property for which a special use permit is sought may initiate a request for a special use permit.”

2019: March 19 State Street Coffee. LLC (a Hari Group captive) buys 206 E State property for $715,000 from the gas station owner, Angel Associates (CIMA LLC).

2020: Property sold at Sheriff’s Auction for unpaid Property Tax

2023: March, Special Use Drive-through apparently gets a City use permit despite failure to complete IDOT-required safety modifications. Dunkin begins sales. Multiple public ROW encroachment violations exist

In the attached graphic, a Geneva taxpayer will sadly note that in the years following the sale of the property, the tax assessor held the fair market value at the level of about 2012. Tax Increment Financing (TIF) funds were gifted to Hari Group, but no property tax increment was assessed despite the sale of the property for ~$250,000 above the assessor’s “fair market value.” I checked the fair market value on my own home about a block away from Dunkin (~$415,000), which seems to me to be about right. (Zillow estimates the net proceeds from a sale at $425,000, for example.) Oddly, my property taxes keep going up. The Dunkin is taxed at about half the last sale price of $715,000. Plus, the new owner gets a Tax Increment Financing cash gift (and sales tax kickback) even though there has been no tax increment. PLUS, the former owner got a $250,000 Special Use bonus that he did not even apply for!

THIS NONSENSE MUST STOP, or Geneva will be “affordable” only for the politically well-connected. Bear in mind the $715,000 purchase price does not include the value of the re-working done on the building and site. While more akin to putting lipstick on a pig than real capital improvements, the assessor wants to know when you re-roof or re-side your house. And he knows when because he takes satellite spy pictures of your property every spring. If you buy a $1 million house, you will not get a fair market value tax appraisal of $380,000 unless you are Mike Madigan’s cousin.

What the assessor has more trouble discovering is the backroom wink-and-nod funding done via public perks that have cash value. For example: “The applicant is requesting three zoning relief items. Two of the relief items are for Required Landscaping requirements per Section 11-10-5 (parkway trees and interior parking lot landscaping) and the other relief item is for dimensions Off-Street Parking Module dimensions per Section 11-11A-7. The strict application of the code would not allow for the required number of parking spaces on the site. The requested zoning relief would allow the reasonable development of the property.” Then the switch from Bollard posts required by Ordinance 2018-36 to hollow flimsy, fabricated metal posts was tantamount to writing the developer a check for $15,000. What is the cash value of the unauthorized “reliefs”?

The “Special-Use” section of the Geneva Municipal Code has no provision for “reliefs,” and the Code demands strict compliance with all nine special use standards.

Ordinance 2018-36 trips and face plants on its first “Whereas:”

“WHEREAS, an application was duly filed with the Plan Commission of the City of Geneva on the 6th day of June 2018, by Eric Carlson on behalf of The Hari Group – Raj Patel (hereinafter referred to as “DEVELOPER”), requesting a Special Use for a drive-through restaurant for the property located at 206 E. State, legally described at Exhibit “A” attached hereto and made a part hereof, hereinafter referred to as the “SUBJECT REALTY”;

The applicant was not the owner and was not lawfully permitted to “duly file” an application for a Special Use Permit.

Is there no fraud investigation unit at the Kane County States Attorney’s Office? Does a “wink and nod” unwritten tenet exist that anyone with their snout alongside the State’s Attorney’s in the Kane County public trough gets a “get out of jail free” pass?

The Sage of Sandholm Street and I were conversing many years ago about a local neighborhood issue. I remarked, “Well, Gordon, you know when the City gets involved, it makes winners and losers.” He gently corrected me. He said, “Doc, you are half right. But actually, when the City gets involved, it makes losers of everyone.” The Sage lives in Julius Alexander’s old house that was built across State Street from the Dunkin’ in about 1839. The Sage moved the Alexander house decades ago from State Street to Sandholm Street to a large lot. He also has close personal ties to the Mill Race Inn site that go beyond Julius Alexander. That is a story for another time.

The garish Dunkin’ spectacle on public display at the southeast corner of Crissey Avenue and E. State Street on Geneva’s east side tells a story of official municipally sponsored decline and decay. This descent into a blighted state is accelerating because of an illiteracy problem at Geneva City Hall. An example of this comprehension deficit can be found by examining two declarative sentences taken from Geneva’s Municipal Code that are written in the English language: 1) “The proposed building, other structures and use comply with any and all regulations, conditions or requirements of the city applicable to such building, structure or use;” and, 2) “It shall be unlawful for any person to erect or maintain any building or structure which encroaches upon any public street or other property.”

The first sentence is Standard Eight of the nine mandatory standards in Geneva’s Special Use provision, contained in Title 11, Zoning. The second sentence is a regulation drawn from the Geneva Municipal Code, Title Eight, Public Ways, and Property. No dispute can arise over whether the Green Wall of Crissey Avenue encroaches into the public right of way of Crissey Avenue. This encroachment is depicted in Geneva Special Use Ordinance 2018-36, which allowed a special use drive-through after the mayor, who only votes when a tie exists, voted to pass the ordinance. Now, “any person” commits an “unlawful” act when that person “maintain(s)” a wall that encroaches upon the public right of way of Crissey Avenue.

What would Forrest Crissey say about this? After all, he wrote the book “Tattlings of a Retired Politician.” Until recently, a Genevan ascending the East side Hill passed the first home where Forrest and Kate Shurtleff Crissey lived as renters. That home, also known as the Miller-Gully House, was allowed to deteriorate under the watchful eye of a Geneva code inspector and then was demolished. The next home up the hill to the east, the Widow Stokes Home, also recently destroyed, was where August Drahms grew up. Literate Genevans might know that Drahms wrote the first American textbook on criminology.

If the reader suspects that the two cited provisions of the Geneva Municipal Code have been cherry-picked, the reader is encouraged to read “Section 11-1-2: – Interpretation.” This section will explain which provisions “shall govern.” Also included in the Code is a definition of “shall:” “May/Shall: The word “may” is permissive; the word “shall” is mandatory.”

Nowhere is the honest enforcement of plain code language more critical than in older neighborhoods where diversity in home size, lot size, and affordability is coupled with substandard infrastructure and governmental mischief. When the property rights of this diverse group of owners are ignored in favor of large corporate recipients of public money gifts such as sales tax kickbacks, TIF, grants, and wink and nod gratuitous zoning “reliefs,” demolition follows. For example, the Dunkin green wall stands while unlawfully encroaching the Crissey right of way, but the historic affordable home in the picture does not. Over the past couple of decades, the City of Geneva’s slipshod wink and nod “bending” of zoning rules has nearly destroyed my neighborhood via demolition by neglect.

Reflections on the Destruction of Verbatim Records of Geneva City Council Closed Sessions – March Madness is Upon Us but Madness is Always in Season at Geneva City Hall

The legendary basketball coach John Wooden said: ” “The true test of a man’s character is what he does when no one is watching.” Having been a high school basketball player (the poorest one on a poor (1-19) 1964 HS team), I followed the game devotedly. That same year (1964), Wooden’s UCLA Bruins were 30-0. Coach Wooden, an English teacher, gave sage advice on many topics. 103 Unforgettable John Wooden Quotes – Addicted 2 Success

In 1963, I followed the fortunes of Coach Mel Johnson’s Elite Eight Geneva Vikings. Coach Johnson was a friend of my father’s, and we attended some games in the Mack Olson Gym, built in the 1950s via collaboration between the Geneva Park District and School District 304 – imagine that. The project was completed without even a single closed-session meeting. The Mack Olson Gymnasium name came later. Mack Olson was a member of the Geneva HS Class of 1960 and was a standout basketball and baseball player. He was a founder of the Geneva Academic Foundation, and, like Gregg Nelson, was a banker.

The ’63 team was a pleasure to watch – they played as a team and were fundamentally sound. Bob Johansen, later an Illini starter, seemed like a superstar to me. Truth be told though, I thought the Viking teams of a couple of years earlier were better with Haskell Tison (he started at Duke and was drafted by the Celtics – see reference to “Hack Tison” in John Wooden’s Wiki Bio), Mack Olson, Gregg Nelson, and a younger Johansen.

For example, the ’61 Vikings won the Hinsdale Regional Championship by defeating Aurora West, Aurora East, and, in the title game, St. Procopius (73-50) (who had earlier beaten Naperville 50-48). Geneva’s balanced scoring was typical in the final game: Tison 20, Nelson 17, Johnson 15, Benson 12, Weeks 3, Arbizzani 2, Johansen 2, Junkins 2.

Geneva lost a heartbreaker in the Sectional.

WHEATON (84): Pfund 38, Hutchinson 13, Fitzsimmons 11, Jones 8, Kee 6, Tichava 6, Close 2.

GENEVA (83): Tison 32, Nelson 21, Johnson 16, Benson 8, Cox 3, Junkins 2, Arbizzani 1.

Who was this villain Pfund who scored 38 points before the 3-point shot? His first name was John, and he was the son of Lee Pfund, the Wheaton College basketball and baseball coach. Some of us remember Lee (LeRoy Herbert Pfund died at 96 in 2017) as a pitcher for the Brooklyn Dodgers in 1945. Leo Durocher, of the Cubs’ infamous 1969 collapse, was the Dodger manager who gave Pfund his first start. Lee was a teammate of Jackie Robinson. In the Sectional Final against Morton, John Pfund scored only 12 points, most late in the game when it was out of reach. The defense-oriented Morton Mustangs (my wife’s alma mater) crushed the run-and-gun Wheaton Tigers 64-46. Randy Pfund, John’s younger brother, went on to become the coach for the Los Angeles Lakers and general manager of the Miami Heat.

Haskell Tyson (6′ 10″) fouled out in the Sectional with 3:53 left in the fourth quarter and Wheaton leading 74-69. Geneva was vying to become only the second team to come out of an Illinois “small school” District Tournament (the “play-in” to the Regionals) to make it to Champaign and The Elite Eight. The Sweet Sixteen Tournament had been reduced to eight in 1956. With 37 seconds left, Geneva’s Bob Cox sank the first of two free throws to make the score 82-81, but he missed the second. Robert “Bob” Cox was another State Bank of Geneva executive and a founder of the Geneva Academic Foundation, among many other things. Geneva’s John Johnson snared Cox’s rebound. His potential game-winner put-back shot was partially blocked with no foul called, and the Tigers got possession. Wheaton’s Chuck Close hit a short jumper with less than 20 seconds left to make the score 84-81 Wheaton. Gregg Nelson countered with a long jumper that would have been a three in another era. But then, of course, Pfund would have scored 50+. Time ran out.

I’ve always felt some bitterness toward Wheaton. But then again, I remind myself that Wheaton’s Red Grange scored 10 points after a touchdown, i.e., PATs, against Batavia HS in 1920. This is Batavia’s only entry in that record book. Geneva is winning that competition with Batavia by a score of +1 to -1. Mike Ratay scored 47 touchdowns for Geneva in 2008. IHSA IHSA Boys Football All-Time Individual Records (Scoring Offense)

I knew both Mack and Gregg. Mack died in 1996 while still at the top of his game. He was a behind-the-scenes kind of person whose advice was sought by many, including me when I had the privilege to serve on the Geneva School Board many years ago. I played hoops against Gregg once in about 1961. My mother had purchased a square grand piano with two notable characteristics: 1) It was a piano tuner’s annuity (even I could tell it was always out of tune), and 2) the thing must have weighed over half a ton. “Nelson Movers” was located “out west” next to what is now Emma’s Landing and my father somehow conned Art, Gregg’s father, into picking up and delivering the monster piano.

So, Gregg and a couple of guys who closely resembled Charles Atlas showed up at our house on Army Trail Road one warm summer day with the piano. I was in the driveway shooting hoops, of course. I’d like to say I helped move the piano, and I did do so by staying well out of the way. After the heavy lifting was over, Gregg left the two guys inside to place the piano in its correct spot (which never changed thereafter). I challenged Gregg to a one-on-one contest to eleven, reasoning what better time to catch him than after he had just moved an immovable piano. He was up 9-0 (What can I say – he got lucky!) when he let me score a couple of times before he was off in the moving van.

Gregg was a banker, following in the footsteps of his father Art, and his grandfather Walter Nelson at the State Bank of Geneva. I am not related to these stalwarts with whom I share a surname that is especially common in Geneva.

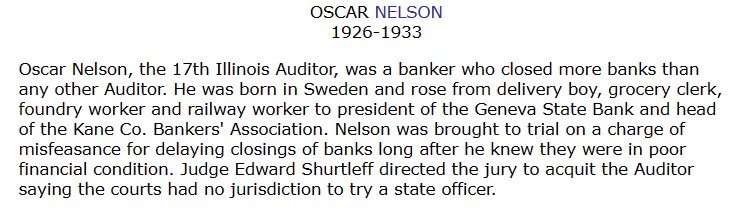

Another Nelson was Oscar, one of the few Genevans whose obituary was published in the New York Times. April 3, 1951. 81772316.pdf (nytimes.com) Oscar was cashier at the State Bank of Geneva in 1920. Later Oscar and his wife Myrtle and his mother-in-law Alice Bennett Gates lived in the Bennett/Gates home at 223 East State just across from the Mayor Burns Dunkin’ at State and Crissey. Oscar, like Walter, Arthur, and Greg was a President of the State Bank of Geneva, though Oscar Nelson was not related to the other Nelsons.

Oscar was not the only Geneva Mayor to be indicted, though his indictment was thrown out by Forrest Crissey’s brother-in-law. Mayor James Herrington was a convicted felon (for assault on his one-armed business partner) when he died in 1839. His son, also Mayor James Herrington, was under investigation for arson-for-hire when he died. His accuser, former Geneva Mayor McChesney (for whom a Geneva HS Golf Tournament is named – he owned the farm that became the Geneva Golf Club) had his own barn go up in flames at about the same time Charles Mussey was accused of torching the Howell Foundry (which then moved to St. Charles). Willis Howell was a McChesney man. The Valley View environmental activist of the 1960s known as the Hot Fox was no relation to Charles Mussey.

Oscar Nelson never tried to hide his judgment calls as the Illinois State Auditor when he allowed borderline banks to stay open in the 1930s. His reports were never redacted or destroyed. He held no secret meetings. He was never accused of political favoritism for the benefit of friends or schoolmates.

Geneva was a community during the Great Depression. Oscar Nelson was a two-term mayor of Geneva before he became a state-wide political figure. Judge Edward Shurtleff was the brother of Kate Shurtleff Crissey, the wife of Forrest Crissey, the Editor of the Geneva Patrol, and the Saturday Evening Post. Oral Geneva legends from the 1950s hold that Oscar Nelson, the banker, quietly and behind the scenes helped many Geneva residents and businesses get through the Great Depression. The same was said of another State Bank of Geneva President, Walter Nelson.

Oscar Nelson ran for Geneva Mayor on an Anti-Burnsian platform. Note his promise to “consult” the people and to be frugal. I wonder what he would have thought of Charettes, land donations, lobbyists, TIF grants, and DEI consultants. Oscar obviously was for equity and inclusion as the 19th Amendment was not signed into law until August 26, 1920. The above article addressed to the “Men and Women Voters” appeared in the Geneva Republican on March 7, 1917.

Geneva Republican, April 5, 1951, p1.

This Italian Villa-style home was built by Charles Bennett in the mid-1860s, not by his nephew -in-law Charles Gates. Charles Gates married Henry Gates’ daughter Alice, who was the niece of Charles Bennett.

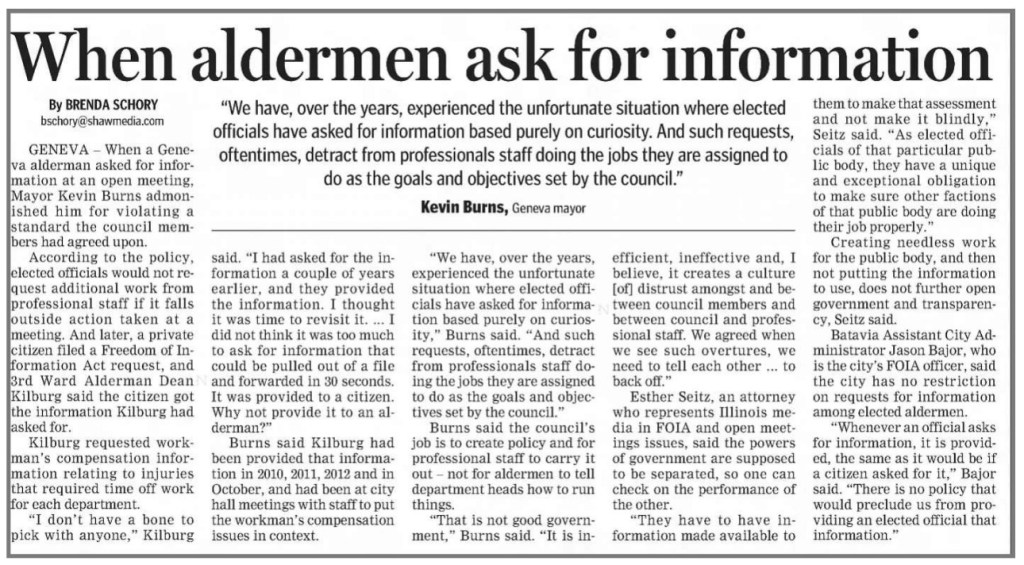

The current Burnsian administration designated me as a “recurrent requester” under the authority of the Illinois Freedom of Information statute. This designation permitted the City of Geneva to embargo my requests for a month. Nothing required the administration to do this. Upon whose authority it was done, I have been unable to learn (in spite of a FOIA request!). I would have thought that the City Council would have had to be involved since I can find no blanket authority in Geneva’s ordinances that grants such powers to the mayor and/or his minions. Of course, in the Burnsian era, secret meetings abound, so one can never be sure of the origin of any city action.

I wear the “recurrent requester” badge with great honor. Yes, I made about fifty requests over a year’s time. I endeavored to make my requests focused and sequential so that I could minimize the City’s inconvenience. Now I understand that my strategy was flawed. I was trying to emulate the Cincinnati Bearcats by employing a methodical process to get to the goal of understanding the ins and outs of how the Geneva city government operates.

The city administration, obviously under the direction of Burns, has made it clear that it does not deign to answer citizen questions. In fact, Burns directed his minions to not even answer aldermanic inquiries.

Mayor Burns couples a policy of forcing cloaked deliberation and then forcing Council decisions “by consensus” on critical issues in secret (with his handpicked staff providing all the Council’s information selectively, while blocking aldermanic access). Then Burns ambushes the victims of these governmental improprieties before those affected (often very few people or an individual) know what is afoot. This has become known as the “Geneva Way.”

I will have to modify my FOIA strategy. The Bearcats led the Loyola Ramblers 48-36 heading into the final 8 minutes in the 1963 NCAA Championship Basketball Game. There was no shot clock in 1963, and no three-point shot – game over, right? Cincinnati had its third straight championship in the bag. Not so fast. Loyola put on a ferocious full-court press and won the game on a Vic Rouse shot at the over-time buzzer.

I had repeatedly asked for the verbatim records (recordings) of several secret City Council sessions. I never received these verbatim records. I have the task now to study the released summary minutes and press on with more FOIA requests, ala George Ireland. I’ll try to become more like a Rambler than a Bearcat when dealing with the City Hall polecats.

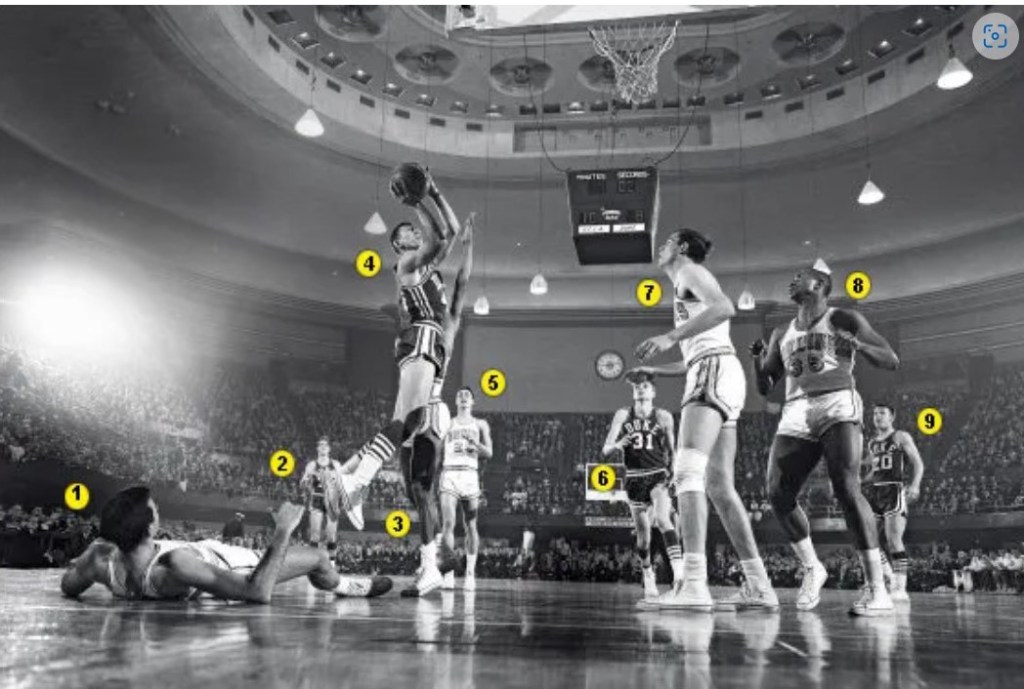

Duke beat Oregon State (83-62) in the 1963 third-place game. Sophomore “Hack” Tison of Geneva (freshmen could not play in 1963) was Duke’s fourth-leading scorer with four baskets and three free throws. He was Duke’s leading rebounder with 11. In 1964, after beating Michigan 91-80 in the semi-final Duke met UCLA in the NCAA Championship Game. The Duke Blue Devils coached by Vic Bubas lost to John Wooden’s Bruins 98-83. Wooden won his first NCAA Tournament. Duke had won the East Regional over Connecticut 101-54! Tison, the Duke starting center, was Duke’s third highest scorer in the final game with 14 points plus 8 rebounds and 2 assists in 27 minutes. Jeff Mullins had 30 points. Drafted by the Celtics, Tison chose a higher-paying job with IBM. He said at the time he was tired of all the traveling and wanted to get on with his life.

Duke’s Jeff Mullins (4) takes a shot in the 1964 NCAA Basketball Tournament final game. UCLA’s Walt Hazzard (3) defends. Geneva’s “Hack” Tison (6) crashes the boards. Keith Erickson (7) went to the 1964 Olympics as a volleyball player. Wooden called Erikson “the finest athlete” he ever coached.

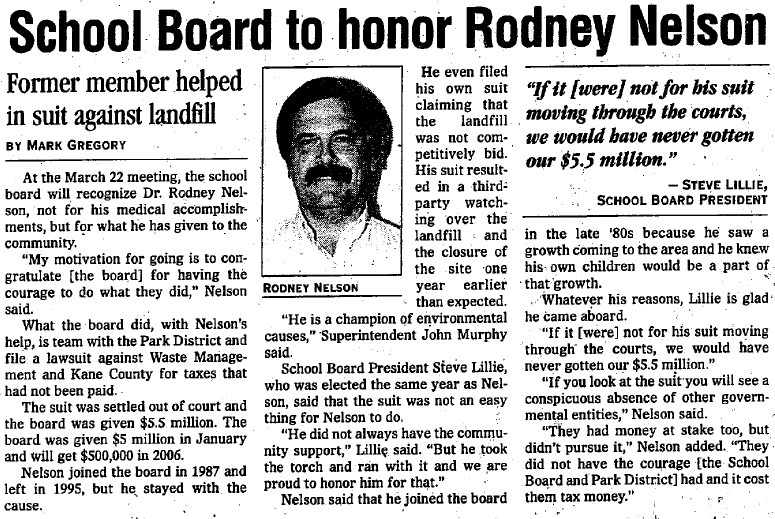

Geneva Republican March 18, 1999

About 30 years ago a local reporter for the Geneva Republican waited around the parking lot of the Kane County Government Center for a closed session of the County Board to end. The young beat reporter interviewed the Batavia representative who told him that the County Board was informed that night by the Kane County States Attorney in a secret session that it was sitting on a “gold mine.” The landfill “enterprise funds” were being used as slush funds for pet projects from canoe shoots to baseball stadiums. The County Board Chairman Warren Kammerer was outraged that the “leak” occurred. His henchmen called for the head of the Batavian (who is one of my heroes). Then someone realized that transparency is a virtue, not a crime.

I read that Republican piece and asked an attorney friend to ask the circuit court to order the release of the tape of that meeting, which the judge did. I went to Lorraine Sava’s office where I was welcomed (Lorraine even entertained my four-year-old daughter and vice versa) while I made a copy of the tape. It took many more years and the efforts of many people, such as County Board Chairman Mike McCoy and Geneva School Superintendent Dr. John Murphy, but the landfill was permanently closed in 2006 instead of 2020, as it was set during the 90s. Geneva District 304 received $5.5 million, and the Geneva Parks got proportionately less in unpaid taxes due. The City of Geneva and Geneva Public Library got nothing as they refused to be parties to the litigation. (I received no money but got priceless satisfaction.)

Oscar Nelson’s frugal “square dealing” of a century ago sharply contrasts with the Burnsian “Geneva Way” of secret sessions and prevarications. Just one example: remember the Burnsian “fact sheet” on Emma’s Landing from July 2020 that claimed that the Burton Foundation was the only applicant for the Eamma’s Landing site in 2019?

The truth is that there was another and better July 2019 offer, submitted by MVAH. MVAH is a LIHTC developer of Senior Housing, a much better fit with Geneva, where District 304 is in Tier 4 for State Funding and 90% of 304’s funding is from local sources. I only know about this offer because I am a “recurrent requester” of the truth. During the flurry of improper secret communications by City staff with the Burton Foundation in the spring of 2020, how many of Mayor Burns’ “overly curious” aldermen even knew about this MVAH offer? How did the Illinois Housing Development Authority conclude that Geneva donated the Emma’s Landing site which resulted in “padding” Burton’s QAP score? The answer is simple, IHDA used email communications between City staff and Burton as the evidence. Now the tapes have been destroyed that “authorized” by a secret City Council “consensus” the improper communications.

Where was square-dealing Oscar Nelson when we needed him most?

What the Geneva City Council does under the direction of the mayor when no one is looking has too often not passed the smell test. And it speaks volumes about John Wooden’s character test. I shall continue to poke at these stench weasels to discover their latest stinker.