Tax Increment Financing (“TIF”) districts and Low-Income Housing Tax Credit (LIHTC) Projects might benefit current residents in some jurisdictions in Illinois. Geneva is not one of those places.

First, some background on TIFs is needed, plus an explanation of the failure of Geneva’s TIF1. Second, the harm done to existing property taxpayers and, more importantly, current school children will be described. The explanation for this net harm within Geneva Community Unit School District 304 can be found by first analyzing the School District’s specific revenue portfolio and then examining how the revenue portfolio interacts with the State of Illinois’ new Evidence-Based Funding formula.

TIF Districts have been around for decades. The enabling statute was designed to provide capital to invest in blighted areas or those at risk for blight. The devil is in the details. For example, a building is “at-risk” for blight based on age alone. Vacant parcels are also considered blighted. Ironically, by distorting property values, TIFs increase tear downs that add to the blight. Five antebellum structures that were the homes of eminent Genevans have been torn down in or near TIF3 in the last couple of years. These very definitions of blight are problematic for older towns like Geneva, and they are lethal for some Geneva neighborhoods, such as Dearborn’s Addition. Sufficient subjectivity exists in the criteria so that “blight” is in the eye of the beholder.

After the City Council defines a TIF district geographically, the property tax for each parcel within the TIF is “frozen” based on its assessment at the TIF’s inception. The various taxing bodies within the TIF district (schools, parks, libraries, townships, etc.) then collect tax dollars based on the frozen assessment for the 23-year life (which can be extended) of the TIF district. The municipal government then collects all the incremental tax revenue generated when the assessment of a parcel increases (“increments”) above the frozen baseline and deposits the proceeds in a TIF fund tied to the TIF district. These funds are supposed to improve infrastructure, but given the fungibility of cash, the TIF fund grants directly subsidize a specific developer.

Many generic risks exist for all TIFs and LIHTCs, but these risks are not borne uniformly. Here are a few of these risks with some Geneva examples:

- Over the past 75 years inflationary years have outnumbered deflationary years 72-3. This creates a powerful driver for increasing property values that favors the municipality’s TIF nominal value but magnifies the tax income losses for the other frozen out taxing bodies. (Inflation is not a law of nature. Steady deflation took place in the U.S. from 1800 to 1850.)

2) Long-term municipal bonds are often sold to directly fund long-life infrastructure assets (sewers, roads, sidewalks, etc.). Current taxpayers can use these assets early in the bond’s life. Bonds sold to provide the cash to fund TIFs immediately benefit only a subsidized developer. But the developer usually must pay income tax on the TIF funds, which reduces the taxpayers’ “bang for the buck” leverage compared to directly funded infrastructure. Tax Increment Financing – What you need to know – REJournals The TIF pot of gold for many taxpayers comes only after 23 years when the increment in assessed valuation suddenly starts flowing back to the frozen-out taxing bodies. Of course, during the 23 years, some taxpayers will be born, some will die (without any “death benefit” from their TIF investment), and many will move in or out of Geneva.

3) The premise of TIFs rests on the “but for” postulate: “But for” the TIF, no development over the 23 years would have happened. This hypothesis is not testable by the scientific method. But Geneva’s TIF1 (1982-2005) and TIF3 (2016-2039) are geographically substantially congruent, covering the same areas on both sides of the river near the bridge. (Tif3 is a gerrymandered, borderline legal oddity primarily focused on The Mill Race Inn and Nottolini Bottling works.) If TIF1 had been successful, why was the same area deemed blighted again only a decade later?

School District 304 publicly opposed TIF3. Mayor Burns went to the Middle School to speak in favor of TIF3 in 2016. His principal argument was that the City had no other tools to stimulate economic development. Hardly a year passed before the Mayor discovered the City could give away sales tax revenues, gift land assets, and waive permit fees to subsidize favored developers.

Here is what the City of Geneva website’s propaganda page says today about TIF1: “What happened during Geneva’s previous TIF[1] district?

Geneva TIF District #1 was established in 1982 and ended in 2005. During that time, the City of Geneva increased the EAV of the TIF district from $1.5 million in 1982 to over $20 million in 2005. When adjusted for inflation, this is over a 600% [nominal: ~1200%] increase in EAV. This was all done without raising taxes.” (FAQs • Geneva, IL • CivicEngage)

The above false claim assumes the “But for” hypothesis is as ironclad as one of Newton’s laws of physics. But the City’s numbers have no meaning in themselves and must be put in context. And the City’s claim that it caused the change in numbers is preposterous, as too many variables were in play. For example, $1.5mil in 1982 would have had to be worth $3.4mil in 2005 if adjusted for inflation to achieve the same buying power. What would have happened if the City of Geneva had invested $1.5mil in the S&P index in 1982? The pot of gold after 23 years would be worth $31.3mil cash in 2005, an increase of 2000%. $1.50 in 1982 → 2005 | Inflation Calculator (in2013dollars.com) From 1982 to 2005 the total EAV in all of Kane County went from $2,097,298,889 to $12,204,273,167, an increase of 482%. StatsGrowthChart1978toPresent.pdf (kanecountyclerk.org)

One significant difference between TIF1 and TIF3 is that TIF1 contemplated immediate sizeable initial capital investment on parcels that were either undeveloped or obviously blighted (the Howell buildings north of State had been largely destroyed by fire earlier). TIF3 (runs from 2016-2039) is a “conservation” TIF that contemplates maintenance, not global redevelopment. The old Nottolini Bottling works in TIF3 may be an exception.

Sizeable and immediate increment in taxes was near-certain in TIF1 because shovel-ready development plans for the west riverbank developments were already in place and approved by the City Council. Interestingly, TIF1 was only “necessary” because a large commercial bank pulled out of a bond deal at the last moment. Read the December 9, 1982, issue of the Geneva Republican for details. Geneva Public Library District – Image Viewer (nmtvault.com)

4) When the City of Geneva freezes the assessed evaluation by creating Tax Increment Financing Districts, the City shifts the burden of the lost tax revenues in the ensuing years in equal proportions to all taxpayers of the other taxing bodies. About 70% of local property taxes go to School District 304. De facto, the Geneva City Council raises taxes for all District 304 taxpayers when it creates a TIF. To the extent the frozen library districts, park districts, townships, etc., overlap District 304, those taxes will also increase. Those affected include residents of parts of Batavia Highlands and parts of Mill Creek and all other residents in School District 304 but outside of the Geneva City limits. Taxation without representation was once celebrated in Boston with a Tea Party.

5) A TIF district creates an associated slush fund susceptible to corrupt practices, such as pay-to-play and kickbacks. These slush funds are like the landfill slush funds once used by Kane County to build a ballpark, canoe shoots, and other political pet projects. Chicago Real Estate Developer Convicted on Federal Fraud Charges for Swindling Banks and the City out of Millions of Dollars in Loans | USAO-NDIL | Department of Justice

Why Did TIF1 Fail to Prevent TIF3?

The short answer is that the Great Recession occurred a few years after 2005. The owners of many TIF1 commercial parcels that TIF subsidized successfully appealed their “increments” in assessed valuation. The only Geneva homeowner to appeal his increased assessment that I know of was Mayor Burns. The Daily Herald from Arlington Heights, Illinois on March 14, 2008 · Page 350 (newspapers.com) These were the “increments,” i.e., the “I” in “TIF” that were supposed to create the pot of gold. But the pot vanished.

TIF1 was implemented in 1982 (when a few citizens, including me, opposed it publicly). That TIF expired in 2005. Here are the tax records for three example properties within or near both TIF1 and TIF3:

(Tax History from assessor’s database):

10-16 West State (a Herrington Inn parcel)

| Year | Base Tax Due | Net Taxable Value |

| 2014 | 76,251.40 | 748,442 |

| 2013 | 54,335.86 | 544,257 |

| 2012 | 56,518.74 | 601,755 |

| 2011 | 83,701.00 | 818,559 |

| 2010 | 119,827.52 | 1,268,993 |

| 2009 | 87,954.26 | 1,003,015 |

| 2008 | 105,883.56 | 1,268,949 |

| 2007 | 96,085.26 | 1,212,217 |

| 2006 | 93,988.24 | 1,132,913 |

27 N Bennett (Geneva Place Retirement)

| Tax History Year Base Tax Due Net Taxable Value 2014 110,681.20 1,140,975 2013 108,409.60 1,140,975 2012 106,636.84 1,194,363 2011 100,674.52 1,199,833 2010 144,810.62 1,875,686 2009 133,022.86 1,875,686 2008 140,332.34 2,032,858 2007 139,901.12 2,032,858 2006 149,670.12 2,116,577 2005 51,043.82 700,442 2004 18,665.50 252,081 |

23 Kane Street (Nelson residence – directly adjacent to TIF3)

| Year | TAX | Net Taxable Value |

| 2014 | 9,987.72 | 102,960 |

| 2013 | 9,782.74 | 102,960 |

| 2012 | 9,757.98 | 109,292 |

| 2011 | 9,754.88 | 116,258 |

| 2010 | 9,384.08 | 121,549 |

| 2009 | 8,739.36 | 123,229 |

| 2008 | 8,541.28 | 123,729 |

| 2007 | 8,151.80 | 118,451 |

| 2006 | 7,919.26 | 111,991 |

| 2005 | 7,578.22 | 103,991 |

| 2004 | 7,320.22 | 98,861 |

| 2003 | 6,965.36 | 94,593 |

| 2002 | 6,891.88 | 90,820 |

So between 2006 and 2014, the taxes on the Nelson Residence went up 28% (no significant capital improvements in that period). This increase is despite the homestead exemption and, after 2011, the senior exemption. Astonishingly, Nelson’s taxes never went down in any year during the “Great Recession.”

Between 2006 and 2014, the tax on a Herrington Inn parcel went down 19%. A drop from high to low of about 55% occurred. This property owner also filed a lawsuit against the City of Geneva when the infrastructure sewer improvements paid for by the diverted taxes of TIF1 catastrophically failed, resulting in flooding.

Between 2006 and 2014, the tax on Geneva Place Retirement went down by 26%. A drop from high to low of about 55% occurred.

During the school district’s scant few actual “pay off” years between the two TIFs 1&3, a homeowner’s share of school taxes went up substantially while the two TIF parcels’ share went down substantially. This is an anecdotal example, but considering the time value of money and risk, TIF1 was a terrible investment for Geneva’s taxpayers and school children between 1982 and 2005.

If TIF3 pays off, the winners will be the taxpayers 16 years from now. If it is unsuccessful, the school children will again be the losers. I submit that the school children of 1982-2005 were the proven losers in TIF1. Again, if TIF1 worked, why was TIF3 created?

TIF3 should be subtitled “The Developers Relief Act of 2016.” The demise and decay of the iconic Mill Race Inn may have been the impetus for the TIF3 plan. Indeed, the initial TIF3 proposal maps included only the east river bank parcels. Our current school children might be better served if the City used its condemnation powers to force at least the demolition of the increasingly dangerous eyesore that was Mill Race Inn. I write this as the person who lives in the house originally built by the second proprietor (John Rystrom, a carriage maker) of the Alexander blacksmith shop that was later the core of the original limestone Mill Race Inn in the 1930s. (The author has owned and lived in three historic antebellum “plaque” Geneva homes: McKinley House, William Conant House, and Hester House. He also successfully prepared and submitted the application for listing on the National Register for the William Moats Farm in rural Ogle County.) https://en.wikipedia.org/wiki/William_Moats_Farm

TIFs are real estate speculations made by amateurs on behalf of taxpayers for the benefit of politically connected developers. Few taxpayers would speculate on lottery tickets with an unknown payoff amount and with the drawing date unfixed decades into the future. Ironically, the original Town of Geneva was platted by land speculators just a few months before the Panic of 1837. Several of them filed for bankruptcy in 1843. One of the speculators, James Herrington, died insolvent and as a convicted felon after he assaulted his business partner, the one-armed Mark Daniels.

TIFs and School Funding in Geneva, Illinois

Understanding why TIFs are harmful in Geneva requires knowledge of the provisions of Illinois’ new Evidence-Based School Funding (EBF) plan.

In Illinois, state money for primary and secondary education is distributed according to two variables: Equalization Formula Grants plus Supplemental Low-Income Grants. The laudable goal of the EBF is to provide adequate funding for each district and each student. The process results in assigning each school district to one of four “tiers of adequacy.”

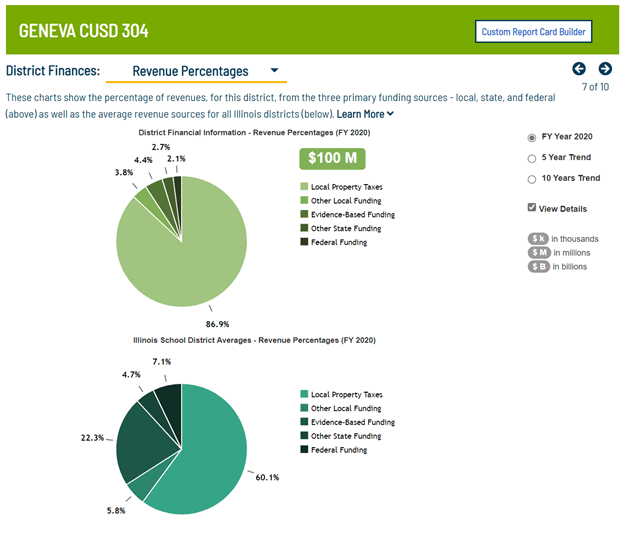

Tier 1 gets the most state money/pupil, and Tier 4 gets the least. Geneva is in Tier 4. The 91% number emerges as the percent of Geneva’s school funding sourced from local taxes (see graph above). The State average is 66% from local sources. The school tax is about 70% of a Genevan’s property tax bill, and about 75% of Geneva’s property tax base is in Geneva homes.

What does this have to do with TIF districts and LIHTC housing projects? The answer is “plenty.”

The ink was barely dry on the EBF legislation when strategies for gaming the formula were implemented. TIFs are the primary gambit. Chicago has 36% of its property tax base hidden or reduced from the State School EBF in 136 different TIFs. Share of City Property Tax Revenues Claimed by TIF Funds Grew 5% in 2 Years: Report | Chicago News | WTTW Geneva’s hidden EAV in TIFs would not be nearly sufficient to get into Tier 3, where EAV per-pupil determines State funding. Geneva would still get the nominal, fixed per-pupil State grant.

Even the short-run impact of a TIF district may be mitigated in some Illinois School Districts (but not Geneva) because Illinois’ school aid formula depends on the property tax base per pupil that compensate school districts, at least to some degree, for the loss of tax base due to TIF. For example, Illinois’ state-aid formula subtracts TIF increments [i.e., “hides” the increment] from the available tax base per pupil to calculate state aid.

The “some degree” of mitigation from a TIF in Geneva is zero since state support amounts to about 4.5% of the total. The sweet spot for this TIF-related mitigating effect on homeowners’ property tax lies somewhere in Tier 2, where State aid provides 40-60% of the total school budget. School districts in Tier 1 have such a small component of local funding that there remains a negligible effect left to mitigate. The local “tax mitigation” that results from hiding TIF properties from the funding formula phases out entirely for wealthier districts in Tier 4 (like Geneva). From the State, Geneva receives a “base grant” of a few hundred dollars per pupil that is fixed. This is analogous to the federal tax deduction for local property taxes that is capped at $10,000. A large percentage of Geneva taxpayers “lose” some of their property tax deduction from Federal Income tax.

Like TIFs, LIHTC affordable Housing Projects like Emma’s Landing in Geneva also serve to hide assessed valuation from the EBF state school funding plan. This is so because the applicable Illinois statute (35 ILCS 200) does not use the fair market value of such projects, but rather uses a tax algorithm based on the LIHTC project’s income. This is really an income tax, not a property tax. Again, for LIHTC projects this mitigating effect on property tax has a “sweet spot” somewhere within Tier 2 or 3 school districts. The mitigation has the same mechanism as TIFs – “hiding” assessed evaluation from the calculation that determines the amount of state aid. For Emma’s Landing This amounts to ~50% subsidy from the other Geneva property taxpayers.

For example, a LIHTC project (Water’s Edge) in Elgin District 46 cost $16+ million to build 50 units but is tax assessed at $3.3 mil and is also in a TIF district. Elgin provides 46% of the support for its schools from local taxes – half the 91% provided by Geneva. Last year, the Water’s Edge project paid school taxes totaling $1700 on all 50 households combined. A single household in Geneva’s Ridgewood neighborhood valued at $172,000 pays $1100 dollars a year in Geneva school taxes.

Water’s Edge, 418 N Center St, South Elgin 2000 Tax Bill – Same Developer as Emma’s Landing

Example of a Ridgewood, Geneva 2000 Tax Bill

Obviously, the Geneva household pays about 40 times what a LIHTC/TIF Water’s Edge South Elgin household pays in school taxes. The latter, of course, pays the tax through rent. Emma’s Landing is a LIHTC project, but it is not in a TIF district.

Property taxes are extremely regressive, that is, they hit lower-income households with limited discretionary income the hardest. If you lose your job, at least you lose your income tax liability. But your property taxes just keep rolling along, sometimes increasing year by year, until you are forced out of your home.

TIFs, Emma’s Landing, and the proposed 250 unit Cornerstone (?LIHTC) project will put upward pressure on Geneva’s school tax levy. If affordable housing is the goal, the City of Geneva should concentrate on putting downward pressure on property taxes. Lower-income households living in $172,000 homes should not be taxed out of town because they are forced to subsidize other lower-income Genevans living in new homes that cost $450,000 each to build.

A tier 4 school district like Geneva 304 (designated by the State as “over-funded” at 105%) accrues none of the TIF or LIHTC “hide-the-EAV” benefits that come through Illinois’ Evidence-Based school funding formula. These benefits accrue to low-EAV per-pupil Tier 2 districts like Elgin 46. TIFs and LIHTCs in Geneva create more problems and higher expenses but few, if any, benefits.

The Geneva City Council’s scramble to accept anything and anybody to give away tax money to is tactically foolish and strategically disastrous. Subsidizing with public money, much of the cash coming from Geneva homeowners, a drive-thru at the top of a hill at a busy un-signaled intersection that is in its 4th year of construction and a LIHTC project tucked up against the RR tracks next to a brownfield of roofless buildings and abandoned vehicles are examples of short-sighted and distorted decisions that are an embarrassment to the community.

Each of Illinois’s 7000 local taxing bodies must consider its unique set of circumstances.

ps: Significant resources are involved here:

Hi! Thank you for getting info out to the public on TIFs. I lead a FB group with over 1,800 followers to oppose a development that will be annexed into Sugar Grove and demanding a TIF that appears to be $127 million per FOIA docs. I need help understanding the effects on the school district to be able to explain this better and prepare post to get people to the Kaneland Board meetings equipped with facts. Kaneland is a tier 3 school. Can you please call me at (630)702-9532?

LikeLike

I have followed from a distance the proposal for the massive development at 47 and 88. For me it was a bit of a deja vu. Several decades ago a developer bought up land southwest of Geneva towards Elburn. Massive housing development seemed imminent, and the Geneva Community Hospital planned a six-story addition. That development collapsed with the housing market in the early 1980’s when mortgage rates reached 18%! I was a member of the Geneva Community School District 304 Board from 1987 to 1995, a period of rapid enrollment growth. The City of Geneva passed “TIF1” in 1980 for the area at the river downtown. A shovel ready plan was approved and bank financing seemed in place. At the last moment the bank pulled out. The Geneva City Council stepped in and passed TIF1 – it was controversial then, and I and many others opposed it. For a few short years the schools received some modest benefit when the TIF expired. But the 2008 housing collapse took away the punch bowl. The TIF recipients’ lawyers were first in line at the assessor’s office, and they obtained large reductions in assessed value. Some of those properties are still paying less tax today than they did in 2005!

LikeLike