The Dunkin Grift Explained

Zoning Fraud in Geneva, Madiganistan

The Crissey/State Dunkin Special Use Permit (Ordinance 2018-36) has an approximate cash value of $250,000. Not a bad return on a speculative grift. But the City of Geneva has been an easy mark for scammers for two decades. The Prairie State Energy Campus is the granddaddy.

The Leaking Underground Storage Tank Property at 206 E State is uninhabitable for residential use. If the reader goes to the Kane County Recorder’s site and enters document 2017K018663, the reader will find an IEPA “No Further Remediation Letter” that contains this restriction on the use of the land: “limitation: The land use shall be industrial/commercial. The groundwater under the site shall not be used as a potable water supply.”

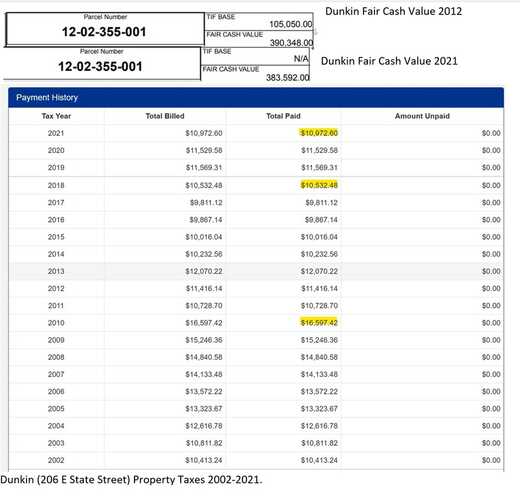

Below is the fair market value of the Dunkin site in 2012 and 2022 and the actual taxes paid from 2002 to 2021. The Hari Group actually skipped paying property tax for a while but bought the property back after it was sold at a sheriff’s sale. Here is the timeline:

2017: Property first becomes saleable for commercial industrial use after TACO review and NFR;

2018: On Nov. 18 City grants a Special Use Permit to the Hari Group, Inc., for a drive-through. This Special Use Ordinance is unlawful under the Geneva Municipal Code, which states, “C. Initiation: The owner of the property for which a special use permit is sought may initiate a request for a special use permit.”

2019: March 19 State Street Coffee. LLC (a Hari Group captive) buys 206 E State property for $715,000 from the gas station owner, Angel Associates (CIMA LLC).

2020: Property sold at Sheriff’s Auction for unpaid Property Tax

2023: March, Special Use Drive-through apparently gets a City use permit despite failure to complete IDOT-required safety modifications. Dunkin begins sales. Multiple public ROW encroachment violations exist

In the attached graphic, a Geneva taxpayer will sadly note that in the years following the sale of the property, the tax assessor held the fair market value at the level of about 2012. Tax Increment Financing (TIF) funds were gifted to Hari Group, but no property tax increment was assessed despite the sale of the property for ~$250,000 above the assessor’s “fair market value.” I checked the fair market value on my own home about a block away from Dunkin (~$415,000), which seems to me to be about right. (Zillow estimates the net proceeds from a sale at $425,000, for example.) Oddly, my property taxes keep going up. The Dunkin is taxed at about half the last sale price of $715,000. Plus, the new owner gets a Tax Increment Financing cash gift (and sales tax kickback) even though there has been no tax increment. PLUS, the former owner got a $250,000 Special Use bonus that he did not even apply for!

THIS NONSENSE MUST STOP, or Geneva will be “affordable” only for the politically well-connected. Bear in mind the $715,000 purchase price does not include the value of the re-working done on the building and site. While more akin to putting lipstick on a pig than real capital improvements, the assessor wants to know when you re-roof or re-side your house. And he knows when because he takes satellite spy pictures of your property every spring. If you buy a $1 million house, you will not get a fair market value tax appraisal of $380,000 unless you are Mike Madigan’s cousin.

What the assessor has more trouble discovering is the backroom wink-and-nod funding done via public perks that have cash value. For example: “The applicant is requesting three zoning relief items. Two of the relief items are for Required Landscaping requirements per Section 11-10-5 (parkway trees and interior parking lot landscaping) and the other relief item is for dimensions Off-Street Parking Module dimensions per Section 11-11A-7. The strict application of the code would not allow for the required number of parking spaces on the site. The requested zoning relief would allow the reasonable development of the property.” Then the switch from Bollard posts required by Ordinance 2018-36 to hollow flimsy, fabricated metal posts was tantamount to writing the developer a check for $15,000. What is the cash value of the unauthorized “reliefs”?

The “Special-Use” section of the Geneva Municipal Code has no provision for “reliefs,” and the Code demands strict compliance with all nine special use standards.

Ordinance 2018-36 trips and face plants on its first “Whereas:”

“WHEREAS, an application was duly filed with the Plan Commission of the City of Geneva on the 6th day of June 2018, by Eric Carlson on behalf of The Hari Group – Raj Patel (hereinafter referred to as “DEVELOPER”), requesting a Special Use for a drive-through restaurant for the property located at 206 E. State, legally described at Exhibit “A” attached hereto and made a part hereof, hereinafter referred to as the “SUBJECT REALTY”;

The applicant was not the owner and was not lawfully permitted to “duly file” an application for a Special Use Permit.

Is there no fraud investigation unit at the Kane County States Attorney’s Office? Does a “wink and nod” unwritten tenet exist that anyone with their snout alongside the State’s Attorney’s in the Kane County public trough gets a “get out of jail free” pass?